SMM, May 8, 2025:

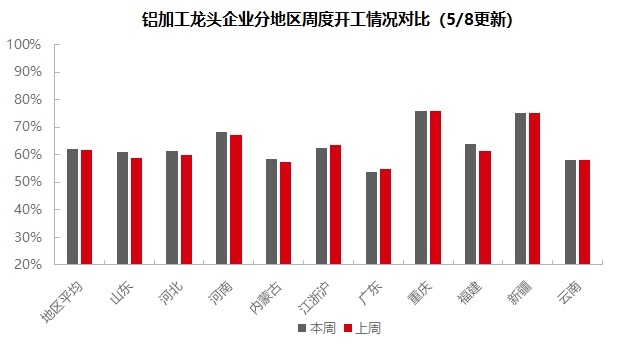

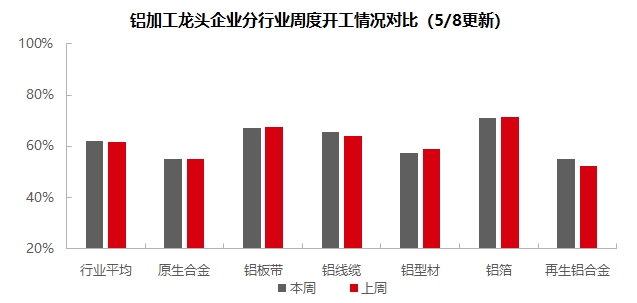

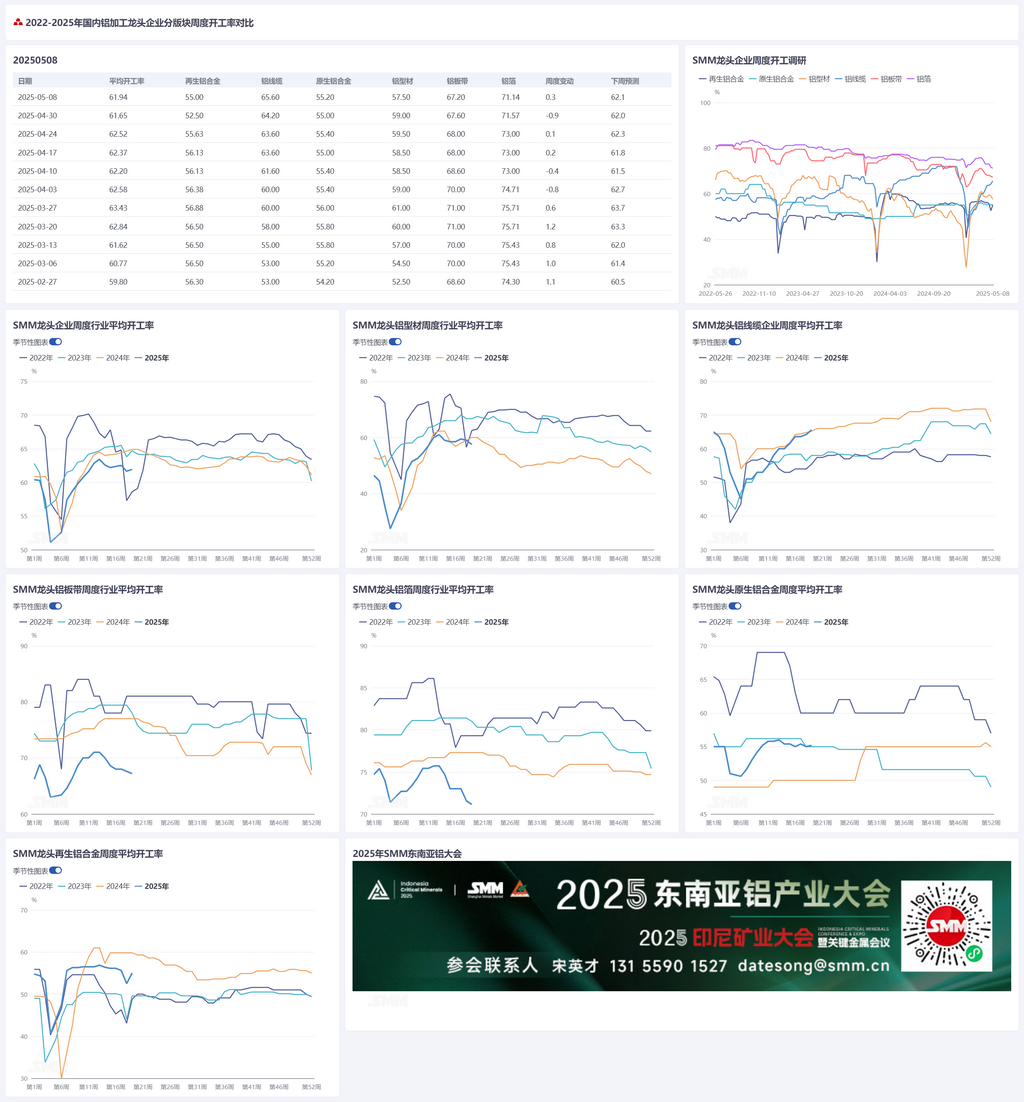

This week, the operating rate of leading enterprises in China's downstream aluminum processing sector rose by 0.3 percentage points WoW to 61.9%. The operating rates across different segments showed a divergent trend: the operating rate of primary aluminum alloy enterprises increased slightly by 0.2 percentage points WoW to 55.2%. Despite maintenance work at some sample enterprises this week, the overall industry performance still exceeded pre-holiday expectations. Orders in early May improved compared to late April, and it is expected to remain stable next week. The operating rate of leading aluminum plate/sheet and strip enterprises fell by 0.4 percentage points WoW to 67.2%. Although enterprises generally maintained normal production during the Labour Day holiday and market demand remained moderate, some sample enterprises faced weak new orders. The operating rate of aluminum wire and cable enterprises increased by 1.4 percentage points WoW to 65.6%. In early May, transmission and distribution orders officially entered the delivery phase, and previously reserved orders began execution, driving production loads to continue rising. With the launch of the second batch of tenders, long-term orders will be effectively connected with existing ones. In the first week after the holiday, the national operating rate of extrusion enterprises declined slightly by 1.5 percentage points WoW to 57.5%. Affected by changes in orders from different end-user automakers, some enterprises reported a slight decline in their operating rates. This week, some PV sample enterprises maintained high operating rates as the frames produced this week could still meet the May 31 deadline. However, some enterprises reported a continuous decline in the proportion of PV production to cope with subsequent weakening demand, while increasing the proportion of other industrial materials such as power pipelines. Building materials enterprises reported weak order growth this week, mainly focusing on maintaining production for existing orders. The operating rate of aluminum foil enterprises fell by 0.5 percentage points WoW to 71.1%, entering the traditional off-season with divergent demand. The operating rate of secondary aluminum enterprises rebounded by 2.5 percentage points WoW to 55.0%, mainly benefiting from the resumption of production at secondary aluminum plants after the holiday. However, the industry's recovery momentum could not be sustained, and it is expected that the operating rate will continue to decline next week. SMM forecasts that the downstream operating rate may rise slightly by 0.1 percentage point next week to 62.1%.

Primary aluminum alloy: This week, the operating rate of leading enterprises in China's domestic primary aluminum alloy sector remained largely stable, rising by 0.2 percentage points WoW to 55.2%. In the first week after the Labour Day holiday in May, the operating performance of domestic primary aluminum alloy enterprises slightly exceeded pre-holiday expectations. During the Labour Day holiday, some enterprises conducted a 10-day maintenance shutdown and planned to resume feeding tomorrow, with limited impact on the overall industry operating rate. After the holiday, enterprises within the sample reported that order performance and operating conditions in early May were basically consistent with or slightly improved compared to late April. On the one hand, there may be opportunities for easing Sino-US trade relations, and it may be prudent for enterprises to maintain the status quo. Additionally, some enterprises have production targets to meet by mid-year, so they are currently focusing on maintaining the current operating levels, with most enterprises in the industry having no production cut plans for now. On the other hand, aluminum prices were in the doldrums in early May, providing some stimulus to downstream consumption of primary aluminum alloys, with domestic rigid demand supporting industry demand.According to the latest SMM survey, the current tariff impact has not yet significantly spread to the production side of primary aluminum alloy. Currently, many large primary aluminum alloy enterprises are still in the order collection phase. The impact on the operating rate of the aluminum alloy industry is expected to be fully evident by mid-May. SMM predicts that the industry's operating rate will maintain a steady and slightly upward trend next week.

Aluminum Plate/Sheet and Strip: This week, the operating rate of leading enterprises in the aluminum plate/sheet and strip sector decreased by 0.4 percentage points WoW to 67.2%. During the Labour Day holiday, leading enterprises in the aluminum plate/sheet and strip sector generally maintained normal production. However, individual sample enterprises relaxed their production pace due to a decline in new orders, resulting in a slight decrease in the operating rate. Currently, the overall market demand remains moderate. The end-use demand from major consumer terminals such as automotive electronics remains relatively stable. However, the traditional consumption off-season has already begun. Multiple enterprises have reported a downward trend in orders on hand, posing a risk of a decline in the future operating rate.

Aluminum Wire and Cable: This week, the operating rate of leading domestic aluminum wire and cable enterprises reached 65.6%, an increase of 1.4 percentage points MoM from before the holiday, continuing the favorable operating trend since Q2. At the beginning of May, the delivery phase for power transmission and transformation orders officially commenced. Coupled with the execution of orders previously reserved by enterprises, production loads have continued to rise. The second batch of tenders for State Grid's UHV materials has been launched, with a total of 147,000 mt of conductor and ground wire orders. The bid opening period is scheduled for May 19, with planned staggered deliveries starting from December 2025, forming an effective linkage of forward orders. The current pullback in aluminum prices has stimulated enterprises to increase their operating rates. Coupled with the accelerated cargo pick-up rhythm of the State Grid and abundant orders on hand, a synergistic effect has been formed. It is expected that the industry's operating rate will maintain a positive trend.

Aluminum Extrusion: In the first week after the holiday, the national extrusion operating rate decreased slightly by 1.5 percentage points WoW to 57.5%. By segment, some leading automotive extrusion enterprises in east and south China reported a slight decrease in their operating rates compared to last week. The main reason is that there have been changes in May orders, with orders from different end-user automakers increasing or decreasing. Some small and medium-sized enterprises in east China will adjust their product mix based on actual order conditions. Regarding PV extrusion, some leading PV extrusion enterprises reported maintaining full production capacity this week. The main reason is that the frames produced this week can still meet the May 31 period. However, according to the SMM survey, some enterprises in Shandong reported that their PV extrusion capacity share has further contracted since entering May. Orders for other industrial materials, such as aluminum alloy pipes in the power sector, are relatively saturated and stable, with an increased share in their product mix. In the construction extrusion segment, some building material enterprises in central and east China reported sluggish growth in new orders this week, with a slight decrease in operating rates. Most enterprises are mainly digesting existing orders. It is worth noting that a few extrusion plants in central China reported obstacles in purchasing raw materials this week. The main reason they reported is the fluctuating decline in aluminum prices this week, which has led to an increase in the reluctance to sell among upstream aluminum smelters and traders.SMM will continue to track the actual implementation of orders across various sectors.

Aluminum foil: This week, the operating rate of leading aluminum foil enterprises decreased by 0.5 percentage points WoW to 71.1%. Recently, the demand for aluminum foil has shown a divergent trend. Demand for battery foil, brazing foil, and other products strongly related to the automotive industry has remained relatively stable, but there is a growing sentiment of weakening subsequent orders. Competition for aluminum foil products with relatively low added value, such as household foil and container foil, has intensified. Production cuts by Tetra Pak and the release of new capacity have also directly led to a sharp decline in processing fees for double-zero packaging foil. With the official start of the traditional off-season, the production enthusiasm of aluminum foil enterprises has been further suppressed due to weakening demand. It is expected that the operating rate of aluminum foil enterprises will fluctuate downward in the future.

Secondary aluminum: This week, the operating rate of leading secondary aluminum enterprises increased by 2.5 percentage points WoW to 55.0%, mainly driven by the resumption of production at secondary aluminum plants after the holiday. However, the industry's warming trend failed to continue. After Labour Day holiday, the effect of the traditional consumption off-season became apparent, coupled with the impact of tariff policies, resulting in a decrease in both domestic and overseas orders. Trading volume in the spot market continued to hover at a low level. In addition, the continuous decline in aluminum prices exacerbated the wait-and-see sentiment among downstream enterprises. Currently, the industry is facing bidirectional pressures: on the supply side, affected by the contraction of raw material circulation, procurement costs for aluminum scrap remain high; on the demand side, it is suppressed by the widening gap in terminal orders. Affected by this, some secondary aluminum plants have reduced their operating levels. It is expected that the industry's operating rate will continue to decline in May.

》Click to view the SMM Aluminum Industry Chain Database

(SMM Aluminum Team)